Web3 Lending Apps: How Decentralized Identity Powers Smarter Loans

Decentralized identity is revolutionizing web3 lending apps, creating a new era of smarter, more accessible loans. The way we borrow and lend money is evolving fast. For decades, traditional banking institutions held the keys to credit, deciding who qualified for a loan & under what terms.

Then came the rise of lending apps, mobile-first platforms that unlocked credit access for millions, using algorithms and digital footprints instead of just FICO scores.

But now, a new wave is forming at the intersection of blockchain technology and financial services: Web3. This decentralized internet is reshaping not just how we transact, but how we trust. And with it comes a powerful concept: decentralized identity (DID).

Here is a look at how lending apps are built on Web3. They offer decentralized identity at the core to create smarter, fairer, and more inclusive loans.

What Is Decentralized Identity (DID)?

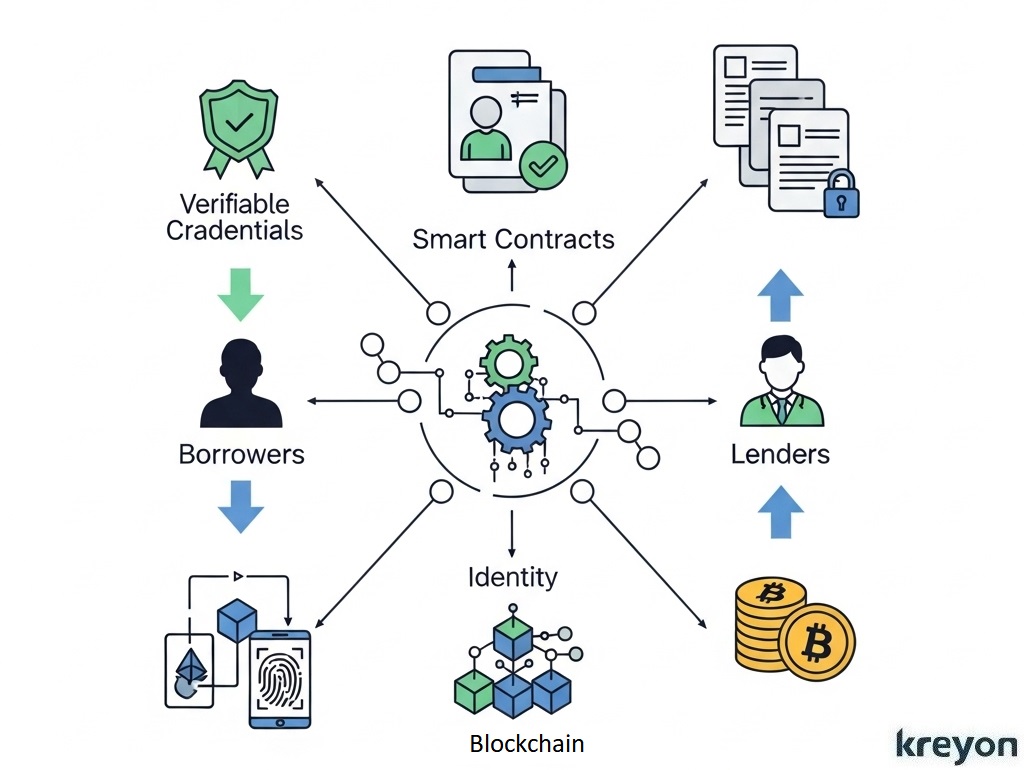

Web3 is about decentralization. It’s about users owning their own data, digital wallets replacing bank accounts, and blockchain-based smart contracts automating trust.

How do you verify someone’s identity and trustworthiness without relying on a central authority? The answer is DID.

Decentralized identity (DID) is a Web3 framework that empowers users to control their personal data using blockchain-based digital identities.

Unlike centralized systems where banks or third parties store sensitive data, DID stores verifiable credentials (VCs), like government IDs, credit scores, or income records, in a user’s blockchain wallet.

These credentials are cryptographically signed by trusted issuers (e.g., banks, governments) and verified via standardized protocols like the W3C DID Specification.

In lending apps, DID replaces manual KYC with instant, secure verification. For instance, a borrower can share a verified income credential from their Ethereum-based wallet without exposing unnecessary details, using zero-knowledge proofs (ZKPs).

An Accenture study found digital identity systems in open banking cut KYC processing times by 60%, a trend Kreyon Systems is now advancing in Web3 lending with custom-built solutions.

It’s a radical shift in trust architecture.

In the context of lending apps, this means you can:

- Prove your income without uploading PDFs of your pay stubs.

- Show a consistent history of on-time rent payments without giving access to your bank.

- Apply for a loan globally, without going through duplicative KYC (know your customer) checks each time.

- All while maintaining privacy and control over your personal data.

Why Web3 Lending Apps Need Decentralized Identity

The emerging generation of Web3 lending apps, built on protocols like Aave, Compound, or Goldfinch, are experimenting with ways to offer credit using blockchain rails. But there’s a problem:

Most decentralized finance (DeFi) lending platforms today are overcollateralized. To borrow $10,000, you might need to lock up $15,000 in crypto. It’s efficient for crypto traders, but it excludes everyday people who need unsecured loans for school fees, medical bills, or starting a small business.

To move beyond overcollateralization, lenders need to trust borrowers.

And that’s where decentralized identity becomes the missing link.

Here’s how:

1. Better Risk Assessment

With access to verifiable, user-controlled credentials, like employment records, rental history, or education, lending algorithms can assess creditworthiness far beyond a FICO score.

For example, a borrower in Nairobi could present proof of steady gig income, verified by a ride-sharing platform, and an on-time payment streak through a local microfinance group. That data, verified and tamper-proof, can inform more nuanced loan decisions.

2. Global Credit Profiles

Decentralized identity allows for portable credit history. A migrant worker sending money home can build credit in one country and use it in another. Students studying abroad can demonstrate financial responsibility across borders.

Credit becomes global, composable, and resilient, independent of any one financial system.

3. Data Privacy and Consent

With Web3 lending apps, borrowers opt-in to share specific data. There’s no black-box algorithm scraping everything you’ve ever done online. Transparency builds trust, not just in borrowers, but in the platforms themselves.

Moreover, decentralized identity minimizes the risk of data breaches. If the lending app doesn’t store your personal data, it can’t lose it.

Case Study:

Kreyon’s DID Integration for a DeFi Lending App:

Kreyon Systems partnered with a DeFi lending platform, LendWeb3, to integrate DID for institutional and retail borrowers, mirroring Aave’s model but tailored for microfinance.

Blockchain: Deployed on Polygon for low gas fees (0.01 MATIC per transaction).

DID Framework: Used W3C DID with uPort resolver for credential verification.

Smart Contracts: Solidity contracts verified VCs using Chainlink oracles, with zk-SNARKs for privacy (e.g., proving income > $20,000).

AI Risk Model: Kreyon’s LSTM-based AI analyzed 10,000 data points (e.g., transaction history), achieving 88% default prediction accuracy.

Wallet Integration: Supported MetaMask and Trust Wallet via Web3.js, with multi-signature security for loans > $50,000.

Results: Approval Time: Cut from 36 hours to 7 minutes for 85% of loans.

User Growth: Onboarded 15,000 users, including 40% gig workers, in 6 months.

Security: Zero data breaches, with ZKPs ensuring privacy.

Cost Savings: Reduced KYC costs by 45%, enabling 2% lower interest rates.

Technical Challenges

Bringing decentralized identity to lending apps isn’t just a matter of plugging in new code. There are real challenges.

For decentralized identity to work, ecosystem adoption is key. Lenders, regulators, and users all need to recognize and trust the credentials. That requires education, standards, and infrastructure.

Adoption: Users may lack blockchain wallet familiarity. Solution: Kreyon Systems builds intuitive mobile apps with React Native, offering tutorials and QR-code wallet setup.

Regulatory Compliance: Varying KYC/AML laws. Solution: Kreyon’s modular compliance engine adapts to 50+ jurisdictions, integrating with Chainalysis for AML checks.

Interoperability: Limited DID standard adoption. Solution: Kreyon supports multi-chain DIDs (Ethereum, Solana, Hyperledger) via DIF Universal Resolver.

Scalability: High gas fees on Ethereum. Solution: Kreyon uses layer-2 solutions like Polygon, reducing costs by 90%.

Lending has always been about trust. Traditional banks used brick-and-mortar branches. Fintech apps used data science. Now, Web3 offers a new model: decentralized, user-owned trust.

By combining lending apps with decentralized identity, we’re building more than just a new financial product, we’re constructing a new social contract.

One where your data is your asset. Your identity is your passport. And your financial future isn’t dictated by a score you can’t see, but by credentials you control.

The future of lending isn’t just digital. It’s decentralized and happening now.

Kreyon Systems blockchain and AI prowess delivers a scalable, secure platform in DeFi microfinance. If you have any queries or need implementation help, please contact us.