NBFC Loan Automation: How to Automate Loan Approval for NBFCs

For non-bank financial companies (NBFCs), whether consumer lenders, SMB financiers, or specialty credit firms to automate loan approval for NBFCs is no longer optional. It’s foundational to sustainable growth.

Borrowers no longer compare you to the lender down the street, they compare you to the smoothest digital experience they’ve ever had. Investors expect portfolio discipline. Regulators expect traceability and fairness. And competitors are investing heavily in automation infrastructure.

But automation isn’t about speed alone. It’s about building a system where compliance, risk management, and scalability operate together without friction.

Let’s go deeper into what that really requires.

Why NBFCs Must Automate Loan Approval Now

Automation solves three structural pressures facing American NBFCs.

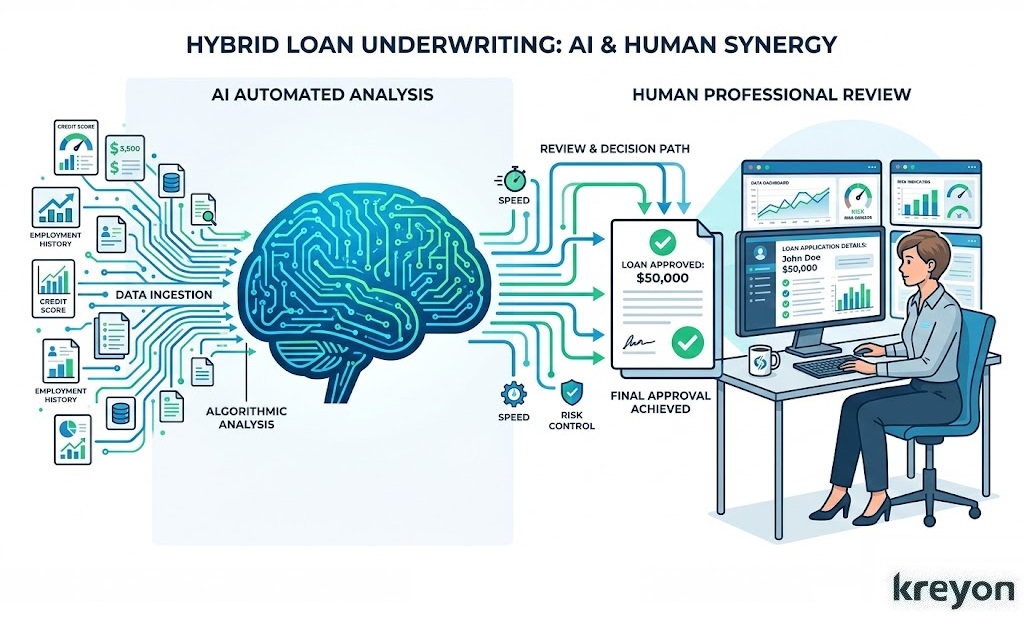

1. Speed Without Weakening Underwriting Discipline

Digital lenders such as SoFi and LendingClub have normalized rapid decisioning. Borrowers expect pre-qualification in minutes and funding within days, not weeks.

But speed alone is dangerous if it bypasses sound credit judgment.

Automation allows you to:

-

Pull bureau data instantly

-

Validate identity in seconds

-

Calculate debt-to-income ratios automatically

-

Trigger conditional approvals based on pre-set rules

Instead of replacing underwriting logic, automation standardizes it. Decisions become consistent, rule-driven, and repeatable. That consistency reduces portfolio volatility over time.

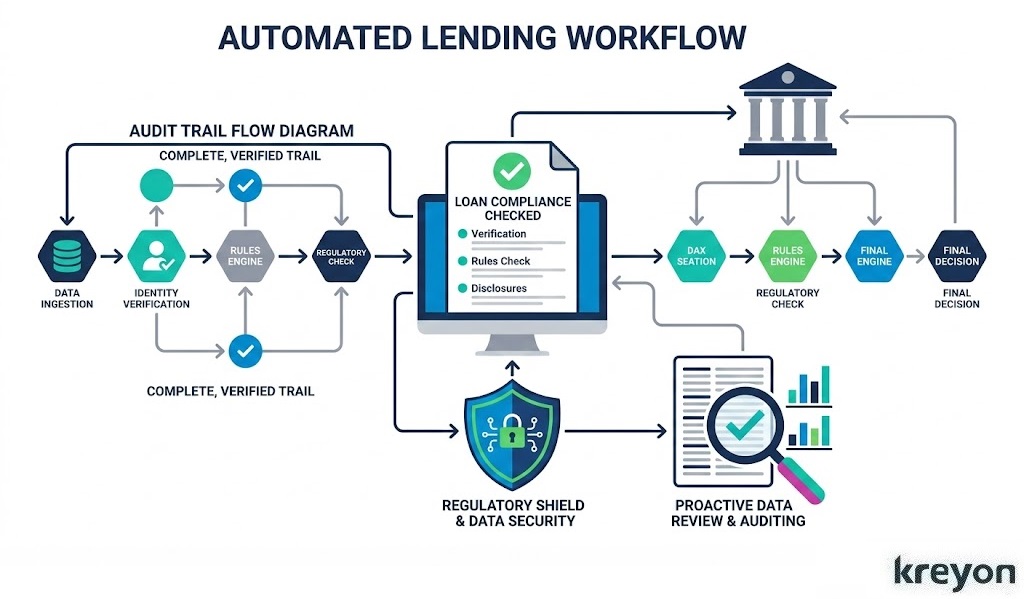

2. Navigating a Fragmented Regulatory Environment

Unlike banks regulated by a single prudential authority, NBFCs must navigate overlapping oversight.

The Consumer Financial Protection Bureau enforces consumer protection standards. The Federal Trade Commission addresses unfair and deceptive practices. States impose their own lending caps, disclosure mandates, and licensing regimes. Privacy laws such as the California Consumer Privacy Act add further complexity.

Manual underwriting increases inconsistency risk. One underwriter may interpret guidelines slightly differently from another. Automated rule engines enforce standardized criteria across every application. More importantly, they log every decision path creating defensible audit trails in case of regulatory review.

Compliance becomes embedded, not reactive.

3. Margin Compression and Capital Efficiency

Rising funding costs and cautious investors mean NBFCs cannot afford bloated operational structures.

Automation reduces:

-

Manual document review time

-

Rework caused by data entry errors

-

Dependency on large underwriting teams for routine cases

This doesn’t eliminate human expertise. Instead, it reallocates talent toward complex cases and portfolio strategy. Operational leverage improves, allowing loan volume to grow without linear cost increases.

In tight capital markets, that efficiency can determine survival.

The Technology Stack Required to Automate Loan Approval for NBFCs

Automation requires layered capabilities working together not isolated tools.

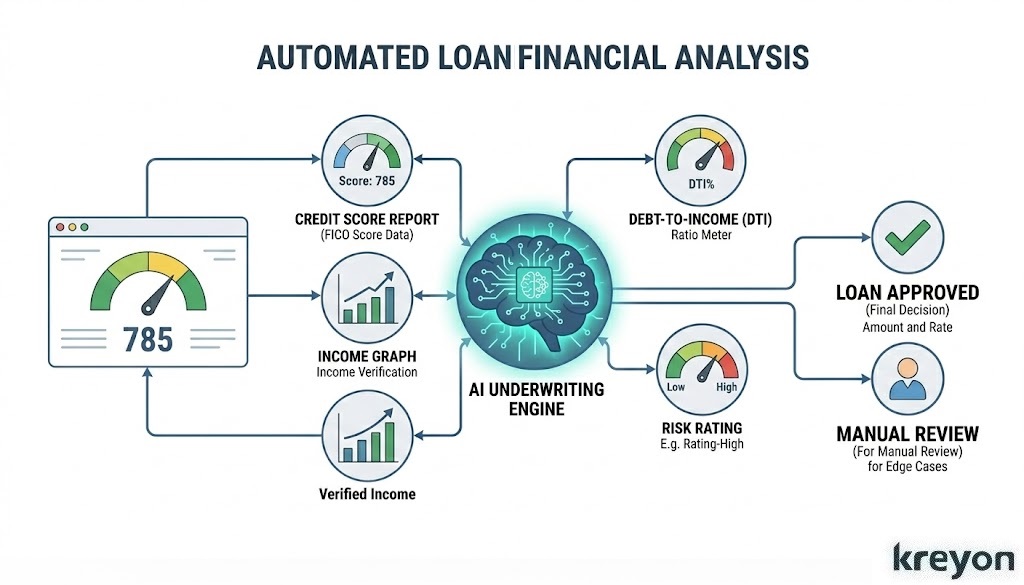

1. Automated Data Aggregation

Modern NBFCs integrate APIs from credit bureaus such as Experian, Equifax, and TransUnion. Instead of manually requesting reports, systems pull data in real time when an application is submitted.

Beyond bureau data, integrations pull:

-

Bank transaction histories

-

Payroll records

-

Tax transcripts

-

Business revenue data

This reduces document fraud and improves income verification accuracy. Structured data ingestion also allows automated recalculations if borrower information changes.

2. AI-Driven Credit Decisioning (With Governance)

AI enhances traditional credit scoring by analyzing patterns beyond static FICO scores.

For example:

-

Income volatility across months

-

Recurring expense ratios

-

Seasonality in small business cash flows

-

Historical repayment behavior clusters

However, in the U.S., explainability is critical. Under the Equal Credit Opportunity Act (ECOA), lenders must provide specific adverse action reasons for denials. AI systems must generate clear, human-readable explanations—not opaque probability outputs.

Model governance should include:

-

Periodic bias testing

-

Validation against historical defaults

-

Documentation of training data sources

-

Independent model review committees

Automation without governance creates regulatory exposure.

3. Income and Cash Flow Verification

Platforms such as Plaid allow borrowers to securely connect bank accounts. With consent, lenders can analyze actual transaction histories rather than relying solely on uploaded pay stubs.

This improves:

-

Fraud detection

-

Accuracy of debt-to-income calculations

-

Assessment of recurring obligations

For small business lending, automated analysis of merchant processing data or accounting software integrations can offer real-time cash flow insights that static tax returns cannot.

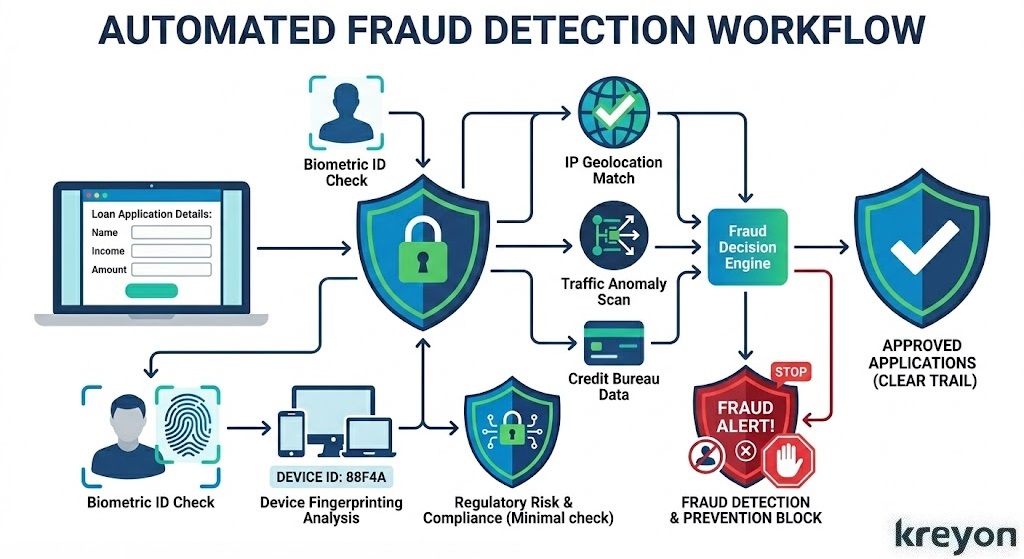

4. Fraud Detection and Identity Verification

Fraud losses in digital lending continue to rise.

Automated systems evaluate:

-

Device fingerprint consistency

-

Synthetic identity markers

-

Geolocation mismatches

-

Behavioral anomalies (e.g., unusually fast form completion)

These signals are difficult to detect manually but highly visible to automated engines trained on historical fraud data.

Continuous monitoring is essential. Fraud tactics evolve rapidly; static rule sets quickly become obsolete.

5. Workflow Orchestration and Exception Handling

A modern loan origination system (LOS) orchestrates every stage:

-

Application intake

-

Data validation

-

Risk scoring

-

Compliance checks

-

Funding authorization

Equally important is exception routing. When applications fall outside predefined parameters, they should automatically escalate to human underwriters with full contextual data attached.

Automation works best when it knows when to defer.

Step-by-Step Framework to Automate Loan Approval for NBFCs

Step 1: Conduct a Process and Risk Audit

Before implementing technology, map your current underwriting flow in detail.

Identify:

-

Manual touchpoints

-

Frequent rework loops

-

High default clusters

-

Compliance pain points

Quantify time spent per application stage. Data-driven diagnostics prevent investing in automation that solves the wrong problem.

Step 2: Prioritize Automation by Risk Impact

Start where automation delivers measurable gains with minimal regulatory complexity.

Examples:

-

Automated bureau pulls

-

Rule-based debt-to-income thresholds

-

Auto-decline for clear policy breaches

Gradual expansion reduces operational disruption and allows iterative refinement.

Step 3: Build Tiered Decision Frameworks

Not every loan requires equal scrutiny.

For example:

-

Consumer loans under $10,000 with high credit scores → Fully automated approval

-

Mid-tier loans → Automated scoring + conditional documentation review

-

Large commercial loans → AI-assisted but human-led underwriting

Tiering protects portfolio quality while maintaining speed for low-risk segments.

Step 4: Establish Model Risk Governance Early

Even if not required by regulation, formal model oversight strengthens credibility.

Governance should include:

-

Annual back-testing against actual defaults

-

Monitoring for disparate impact

-

Documented change logs for algorithm updates

Proactive oversight reduces the likelihood of enforcement action and builds investor confidence.

Step 5: Manage Organizational Transition

Automation alters roles.

Underwriters evolve into:

-

Risk analysts

-

Exception reviewers

-

Portfolio strategists

Invest in training programs that help teams interpret AI outputs and understand automated logic. Cultural alignment is as important as system implementation.

Common Pitfalls When Automating Loan Approval

Fair Lending Risk

AI can inadvertently correlate with protected characteristics. Regular statistical testing is essential to ensure compliance with federal fair lending laws.

Ignoring bias monitoring can lead to enforcement penalties and reputational harm.

Model Drift During Economic Shifts

Interest rate changes, unemployment fluctuations, or sector downturns alter borrower behavior. Models trained during stable periods may misprice risk during volatility.

Quarterly recalibration and stress testing against recession scenarios are prudent safeguards.

Cybersecurity Vulnerabilities

More integrations mean more access points.

Implement:

-

End-to-end encryption

-

Vendor security audits

-

Real-time breach detection monitoring

Operational resilience is part of credit risk management.

The Strategic Payoff

When executed correctly, automation delivers:

-

Faster decision cycles

-

Improved borrower experience

-

Reduced fraud exposure

-

Consistent compliance documentation

-

Scalable growth without proportional headcount increases

In competitive credit markets, operational excellence compounds. Efficient systems free capital for innovation and market expansion.

Final Thoughts: Automation as Infrastructure, Not Experiment

To automate loan approval for NBFCs is to modernize the core of the lending engine.

It requires thoughtful integration of:

-

Technology

-

Compliance

-

Risk governance

-

Organizational alignment

Automation should not be treated as a fintech experiment. It is infrastructure, foundational to competitiveness in the next decade of American lending.

Begin with a structured audit. Automate where logic is clear and repeatable. Embed governance early. Scale deliberately.

The future of NBFC lending will be intelligently automated. But, humans will be guiding the exceptions that truly require judgment.

Kreyon Systems provides a cutting-edge, customized AI-powered Lending Management System designed to transform your loan lifecycle from days to minutes. For queries, please contact us.